- PetroPeak Investments Newsletter

- Posts

- Newsletter April 14, 2026

Newsletter April 14, 2026

John Jordan

April 14, 2026

MARKET PULSE

Oil’s New Risk Premium Is a Reminder of Why U.S. Barrels Matter

Oil has moved sharply higher again, with Brent climbing back above $100 per barrel after the latest escalation tied to Iran and the Strait of Hormuz. The immediate driver is geopolitical, but the market reaction is saying something broader. When global supply routes are threatened, price does not just respond to lost barrels. It responds to the value of accessible, exportable, and politically reliable barrels. That is where the U.S. re-enters the conversation in a much bigger way.

There has also been growing market chatter that more oil tankers are heading toward the U.S. Gulf Coast to load crude and refined products for delivery overseas. Reuters reported that vessel availability on the U.S. Gulf Coast had tightened as buyers looked for replacement supply, while shipping through Hormuz slowed and uncertainty around Iranian exports deepened. In a stressed market, U.S. production is not just abundant, it becomes strategically valuable because it can help backfill disrupted global flows.

That does not mean the U.S. can simply replace the Middle East. There are real constraints. Freight costs rise quickly when tanker availability tightens. Transit times to Asia are longer. Not every refinery can seamlessly swap into lighter U.S. crude. And even with strong export capacity, U.S. barrels cannot fully offset the scale of supply that normally moves through Hormuz. This is less a story of the U.S. taking over the global oil market and more a story of the market paying up for optional supply when geopolitical risk spikes.

For investors, that distinction matters. The latest move in oil is a reminder that domestic production carries a strategic premium during periods of disruption, even if that premium does not last forever. Royalty owners do not need a permanent geopolitical crisis to benefit from this setup. They simply need U.S. barrels to remain relevant, competitive, and in demand when global markets become stressed. That is exactly what recent events have reinforced.

The takeaway is straightforward: higher prices may be driven by war headlines, but the deeper message is about the durable global importance of U.S. oil supply. In times of disruption, the value of domestic barrels rises not only because they are produced, but because they can move. And in today’s market, that flexibility is proving to be a competitive advantage.

Commodity | Current Price ($) | Daily Change |

|---|---|---|

WTI Oil ($) | 99.07 | +2.50+2.59% |

Henry Hub Gas ($) | 2.63 | -0.03 -0.94% |

Current Rig Count(US lower 48) | Week Change | Year Change |

545 | -3 | -38* |

*YoY rig changes include oil rigs -61 and gas rigs +22, +1 misc. Prices are as of 04/13/2026 and sourced from oilprice.com. Rig data is provided by WellDatabase.com and as of 04/13/2026.

ROYALTY SPOTLIGHT

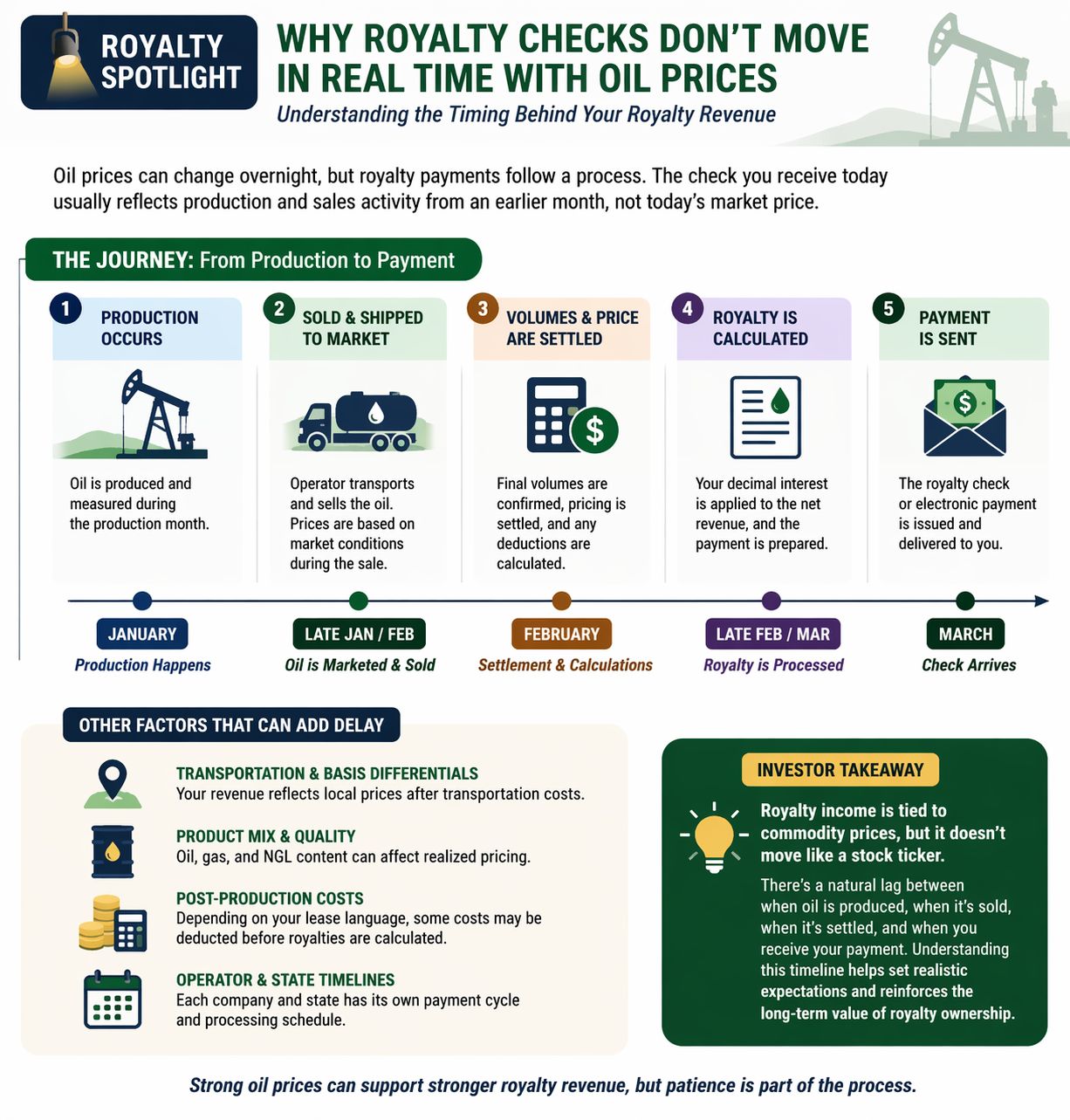

Why Royalty Checks Do Not Move in Real Time With Oil Prices

When oil prices jump, many investors naturally assume royalty income should rise just as quickly. In reality, royalty revenue usually moves with a delay, sometimes by a month or two, and occasionally longer depending on the operator and the state. That timing lag is one of the most important mechanics for royalty investors to understand because it helps explain why royalty cash flow does not always respond immediately to market headlines.

The reason starts with the production cycle itself. Oil and gas are produced during a given month, but that production must first be measured, marketed, sold, and settled before revenue is distributed. The operator or purchaser needs time to finalize volumes, calculate pricing, apply the owner’s decimal interest, and process payments through the revenue system. Only after that process is complete does the royalty owner receive a check. In other words, the payment received today is often tied to production and sales activity from an earlier period, not the current spot price investors may be seeing in the news.

That gap can create confusion during volatile markets. If oil suddenly moves higher because of a geopolitical event, a royalty owner may not see the benefit immediately. The next royalty check may still reflect lower-priced barrels sold in the prior month. The reverse is also true. If commodity prices fall sharply, royalty checks may remain stronger for a short period because they are still reflecting earlier production sold into a better pricing environment. For investors, this is a helpful reminder that royalty income tends to be responsive, but not instantaneous.

There are also other factors that can widen the gap between market price and payment. The benchmark oil price on television is not always the exact price used to calculate royalty revenue. Actual realized pricing may reflect transportation differentials, regional basis, product quality, natural gas liquids mix, and in some cases post-production costs depending on the lease structure. That means royalty checks are shaped not only by headline commodity prices, but by the specific economics of the underlying property.

For investors, the takeaway is simple: royalty income is tied to commodity markets, but it does not behave like a real-time stock ticker. It moves through an operating and payment cycle that can temporarily smooth or delay the impact of price changes. Understanding that timing is important because it sets more realistic expectations and reinforces a broader truth about royalty investing. The value is not in reacting to every daily move in oil. It is in owning an asset that can participate in long-term production and price exposure without the burden of operating costs or drilling obligations.

Strong commodity prices can support royalty income, but checks do not update overnight. Royalty investing rewards patience and an understanding of how production, sales, and payment timing work together.

Real Assets. Real Income. Real Alignment. |

BASIN FOCUS

Is the San Juan Basin Really Back?

The San Juan Basin is beginning to re-enter the conversation, and that alone is notable for a basin many investors have long viewed as mature, legacy-heavy, and largely overshadowed by newer horizontal oil plays. Recent operator updates and public development plans suggest there is more life in the basin than the market may have been giving it credit for. The question, however, is not whether San Juan is suddenly “back” in the same way as the Permian, DJ, or Uinta. |  The more important question is whether select parts of the basin are becoming competitive enough to justify renewed attention. |

That distinction matters.

What appears to be emerging in the San Juan is not a broad basin-wide resurgence, but a more targeted story centered on specific fairways, especially the Mancos gas window and certain southern-rim oil targets. Operators including Mach Natural Resources, Enduring Resources, LOGOS Energy, and Hilcorp are helping shape that narrative, with recent activity suggesting that modern horizontal development can unlock stronger performance than many would expect from a basin with such a long production history. In that sense, the San Juan story is not simply about an old basin trying to reinvent itself. It is about whether overlooked rock, supported by existing infrastructure and lower base declines, can compete for capital when developed with a more modern approach.

Even so, investors should be careful not to overstate what is happening.

The San Juan Basin is still not a direct peer to the premier development windows of the Permian, DJ, or Uinta. Those basins continue to dominate because they combine scale, repeatability, and stronger visibility on future inventory. San Juan’s renewed momentum looks far more selective. The opportunity appears real, but concentrated. That means the basin likely deserves a new lens, though not a blanket re-rating. The winners here will likely be the operators and acreage positions that can combine attractive entry points with strong well results, existing takeaway, and durable cash flow characteristics.

For royalty and mineral investors, that is where the story becomes interesting.

A basin does not need to be the next Permian to matter. In some cases, the better investment opportunities are found where the market is still catching up, where infrastructure is already in place, and where selective development can create meaningful value without requiring top-of-market acquisition pricing. San Juan may fit that description in the right areas. It is still an older basin, but it may also be one where the right rock and the right operators can create a very different outcome than the legacy label implies.

The takeaway is straightforward: the San Juan Basin deserves to be reviewed again, but with discipline. This is not a basin-wide renaissance story. It is a selective opportunity story, and those are often the ones most worth watching.

INVESTOR ADVANTAGE

Commodity Exposure Without Operating the Business

One of the clearest advantages of royalty ownership is that it allows investors to participate in oil and gas economics without taking on the burden of running an operating business. That distinction becomes especially important during volatile markets like the one we are seeing today. Oil prices may rise on geopolitical disruption, tanker markets may tighten, and refining margins may shift quickly, but public operators and downstream companies still have to manage the operational complexity that comes with those changes. Royalty owners do not.

That simplicity matters.

An operator must navigate drilling costs, service inflation, transportation constraints, hedging decisions, staffing, equipment availability, and the day-to-day challenges of developing and producing wells. Refiners and midstream companies face their own complications tied to margins, logistics, maintenance, and market dislocations. Even in stronger price environments, those moving parts can make financial performance less straightforward than headline commodity prices might suggest.

Royalty ownership works differently. A royalty interest is tied to production revenue, but it does not carry the capital obligations, operating expenses, or execution risk that come with drilling and running the asset. Investors are not responsible for building the well, managing the frac crew, marketing the barrels, or absorbing cost overruns. They benefit from the production and revenue stream while remaining outside the operating chain.

For investors, that can be a powerful combination. Royalties offer exposure to the long-term value of oil and gas production while avoiding much of the complexity that can make direct operating businesses difficult to manage and underwrite. This does not remove commodity risk, but it does create a cleaner ownership structure, one where the focus stays on asset quality, operator strength, and cash flow potential rather than on the operational headaches behind the scenes.

In a market where headlines can change quickly and execution challenges can weigh heavily on operating companies, that simplicity is part of the advantage. Royalty owners are not betting on their ability to run an oilfield. They are investing in the value of production from it.

Royalty ownership offers exposure to energy production without the capital intensity and operating complexity of running the business, which is one reason the model can be so attractive in uncertain markets.

LOOKING AHEAD

Will Higher Oil Prices Trigger More U.S. Activity, or Just More Caution?

The next big question for the market is whether the recent surge in oil prices becomes a short-lived geopolitical spike or the start of a more durable shift in producer behavior. So far, the industry response has been measured. Many operators remain cautious about chasing higher prices too quickly, especially after several years of capital discipline and volatile commodity swings. But there are early signs that the conversation may be changing.

Harold Hamm recently indicated that Continental plans to increase rigs across U.S. basins, a notable signal from one of the industry’s most outspoken voices. He may prove to be earlier and more aggressive than many of his peers, but he does not appear to be operating entirely alone. Recent industry surveys suggest smaller producers are becoming more willing to add activity if stronger prices hold, while larger companies remain more hesitant to make immediate moves. In other words, the market may be approaching an inflection point, but it has not clearly crossed it yet.

That is what makes the coming weeks so important. If oil prices remain elevated long enough, more operators may begin to cautiously add rigs, complete wells, and revisit development plans that looked too conservative just a month ago. If prices retreat, many of those plans may remain on hold. For investors, this is a reminder that the next phase of the story is not just about where oil trades, but about whether producers believe the move is durable enough to justify action.

The takeaway is simple: watch not just the price of oil, but the behavior of operators. The market’s next clue will come from whether higher prices begin to translate into real activity growth or remain a temporary signal that most companies are still unwilling to chase.

Ways to Connect with Us:

Email: [email protected]

Website: www.petropeakinvest.com

Schedule a Call: Book a time here

Follow us on LinkedIn and socials: PetroPeak Investments LLC, @petropeakinvest

Whether you’re exploring royalties for the first time or looking to deepen your exposure, PetroPeak can guide you through every step from understanding the asset class to participating in high-quality, cash-flowing deals.

Because at PetroPeak, it’s about more than just investing. It’s about building long-term income you can count on.