- PetroPeak Investments Newsletter

- Posts

- Newsletter Feb 17, 2026

Newsletter Feb 17, 2026

John Jordan

February 17, 2026

MARKET PULSE

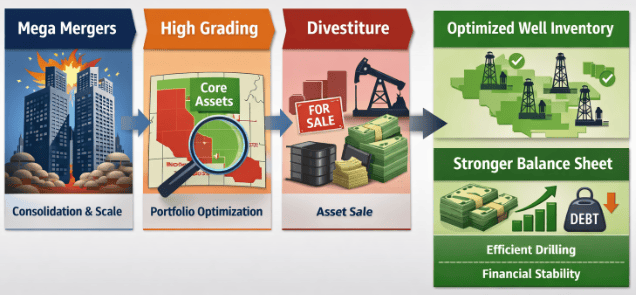

Mega Mergers, Asset Sales, and the Next Phase of U.S. Shale

For the past several years, the dominant story in U.S. oil and gas has been consolidation. Large public companies have combined balance sheets, expanded drilling inventories, and assembled multi-basin portfolios at unprecedented scale.

Companies such as ExxonMobil, Chevron, Devon Energy, SM Energy, and Ovintiv have all participated in this wave. The objective was clear. Secure long runway drilling inventory, improve operational efficiency, and enhance shareholder returns through scale. However, the latest headlines suggest the industry may be entering a new phase.

Recent reporting from Reuters and Hart Energy indicates: ExxonMobil’s XTO unit has been marketing select Eagle Ford assets, SM Energy is exploring a sale of its Eagle Ford position following its merger activity, Ovintiv has launched a divestiture process for certain Anadarko Basin assets in Oklahoma as part of a portfolio transformation.

At the same time, major transactions are still occurring. Devon Energy recently announced a combination with Coterra Energy, reinforcing that large scale mergers remain part of the landscape. So what is happening?

From Acquisition to Optimization

The current trend does not signal an end to consolidation. It signals a transition. The first phase of consolidation focused on assembling acreage and building scale. The second phase is about refining portfolios. After combining companies, management teams are asking a more disciplined question. Which assets truly fit our long term capital allocation strategy?

Large public companies operate under strict financial frameworks. They must maintain investment grade balance sheets, deliver consistent free cash flow, and sustain dividends and share repurchase programs. When leverage increases following a merger, divestitures often become the fastest path back to targeted debt levels.

In addition, operational focus matters. The most successful shale programs operate like manufacturing systems. Standardized well designs, predictable geology, and concentrated infrastructure drive repeatable results. Assets that introduce complexity or sit outside the core development focus can be labeled non-core even if they remain economically viable. This dynamic helps explain why quality assets in places like the Eagle Ford or Oklahoma’s Anadarko Basin are coming to market.

What This Means for Opportunistic Capital

When large operators high-grade portfolios, opportunities often emerge for companies with different financial expectations. For a global major, an asset may be too small to move the needle. For a private operator or royalty investor, that same asset may represent a meaningful and cash flowing opportunity.

There are three reasons this matters:

Valuation resets can occur when sellers prioritize speed and balance sheet improvement over maximum price.

Mature producing assets that no longer fit a growth narrative can generate attractive cash yield for buyers focused on income.

Smaller companies can apply focused operational attention to assets that were previously overshadowed inside large portfolios.

In other words, what is non-core to one company can be core to another.

Not the End of Mergers, but a Maturing Cycle

It would be premature to declare the mega merger era finished. Large scale transactions are still taking place, and capital discipline remains central to corporate strategy.

What we are seeing instead is a maturing cycle. Consolidation created scale. Now the industry is refining that scale to align with return on capital, balance sheet strength, and operational focus.

For disciplined investors, this transition phase often provides some of the most compelling entry points. Assets change hands not because they lack value, but because they no longer align with the strategic priorities of their current owner.

As history has shown, capital that can move decisively and underwrite long term cash flow rather than short term narrative often benefits most during these portfolio reshaping periods.

Commodity | Current Price ($) | Daily Change |

|---|---|---|

WTI Oil ($) | 63.73 | +0.84 +1.34% |

Henry Hub Gas ($) | 3.25 | -0.14 -4.44% |

Current Rig Count(US lower 48) | Week Change | Year Change |

551 | +0 | -37 |

*Prices are as of 02/16/2026 and sourced from oilprice.com. Rig data is provided by WellDatabase.com and as of 02/16/2026.

ROYALTY SPOTLIGHT

Non-Core to Them. Core Cash Flow to You.

Recent headlines have focused on large operators marketing assets in places like the Eagle Ford Shale and Oklahoma’s Anadarko Basin. Companies such as ExxonMobil, SM Energy, and Ovintiv are refining portfolios following merger activity and balance sheet priorities. To public equity markets, these are framed as “non-core” asset sales. To a mineral and royalty owner, the interpretation can be very different.

Assets Do Not Become Uneconomic Overnight

When a large company divests acreage, it is usually a matter of capital allocation discipline. Public companies must concentrate drilling capital where it can generate the highest return on invested capital at scale. That often means focusing on one or two primary development engines. Assets outside that focus may still be productive, cash flowing, and supported by existing infrastructure. They simply no longer compete for capital inside a multi billion dollar portfolio.

For royalty owners, this distinction matters. Mineral ownership does not carry operating costs. It does not fund drilling. It does not absorb capital expenditures. It benefits from production regardless of which operator controls the asset.

Operator Transitions Can Be Catalysts

In many cases, divested properties move to companies that specialize in that basin. Smaller operators may: Increase drilling cadence, target overlooked zones, execute workovers or recompletions, and/or optimize infrastructure utilization.

What was non-core to a global major can become core to a focused operator. For the royalty owner, this can translate into renewed development activity layered on top of existing producing wells.

Durability Through Cycles

This dynamic reinforces one of the foundational strengths of mineral ownership. The asset is not tied to a single management strategy or capital framework. As companies merge, divest, and reposition, the mineral interest remains intact. Ownership persists across corporate cycles.

In a market environment defined by consolidation and portfolio reshaping, this stability becomes increasingly valuable. Capital shifts. Strategies evolve. Operators change. The mineral interest continues to generate income from production.

Non-core to them can very well mean core cash flow to you.

Real Assets. Real Income. Real Alignment. |

BASIN FOCUS

The Woodford in the Midland Basin: Emerging Depth, Comparable Results

For years, the Midland Basin has been defined by the Spraberry and Wolfcamp. Those benches built the modern Permian manufacturing model and still account for the majority of horizontal wells drilled since 2020. But attention is increasingly shifting deeper.

Recent coverage in the Journal of Petroleum Technology highlighted the latest U.S. Geological Survey assessment, which estimates mean technically recoverable resources of 1.6 billion barrels of oil and 28.3 trillion cubic feet of gas in the Woodford and Barnett intervals across the Permian Basin. That federal assessment reinforces what operators have been testing in the field.

Hart Energy has also reported that Occidental Petroleum has drilled more than 110 miles of lateral in the Woodford, signaling that this is no longer a fringe target. It is active capital deployment. The question for investors is straightforward. Are the results competitive?

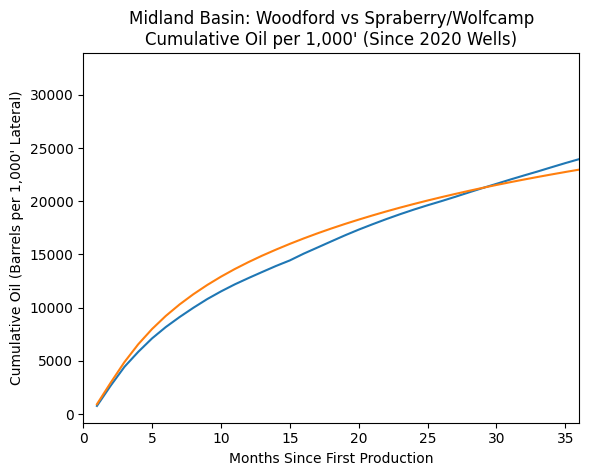

Production Comparison Since 2020

Using data screened from Welldatabase.com, we evaluated all Midland Basin wells drilled since 2020 that: have lateral lengths of at least 8,000 feet, are classified as either Spraberry/Wolfcamp or Woodford, have reached 36 months of production history. This dataset was normalized per 1,000’ of lateral length. Blue is Woodford and Orange is Spraberry/Wolfcamp.

Early production favors the Spraberry/Wolfcamp. By 24 months the gap nearly closes. By 36 months, the Woodford slightly exceeds on a normalized basis. The production curve suggests that while the Spraberry/Wolfcamp may deliver stronger early oil volumes, the Woodford appears to exhibit a flatter decline profile through three years.

The Statistical Reality

There is an important caveat. At the 36 month mark, the dataset includes approximately 6,000 Spraberry/Wolfcamp wells and 30 Woodford wells. This imbalance matters. Thirty wells do not provide basin-wide statistical confidence. The Woodford sample may reflect specific operators, specific counties, or specific depth windows. What this data shows is proof of potential, not proof of full-scale manufacturing repeatability.

Strategic Implications

The Woodford story in the Midland Basin is not about replacing the Wolfcamp. It is about extending stacked pay depth and expanding long-term drilling inventory. For operators, deeper benches provide runway. For mineral and royalty owners, they create additional optionality below existing producing intervals. If Woodford results continue to demonstrate competitive oil recovery per foot with consistent execution, it transitions from secondary target to durable development layer. The next several years of drilling will determine whether it becomes a broad manufacturing bench or remains a selective sweet-spot play. Based on current results, it clearly warrants serious attention.

INVESTOR ADVANTAGE

Optionality Without Capital Risk

One of the most underappreciated advantages of mineral and royalty ownership is optionality. This week’s Basin Focus section highlighted the growing attention on the Woodford in the Midland Basin. Production data from wells drilled since 2020 shows that when normalized per 1,000 feet of lateral, Woodford oil volumes are tracking closely with Spraberry and Wolfcamp results through 36 months. The key investor question is not whether the Woodford replaces the Wolfcamp. It is what this development layer represents for capital efficiency.

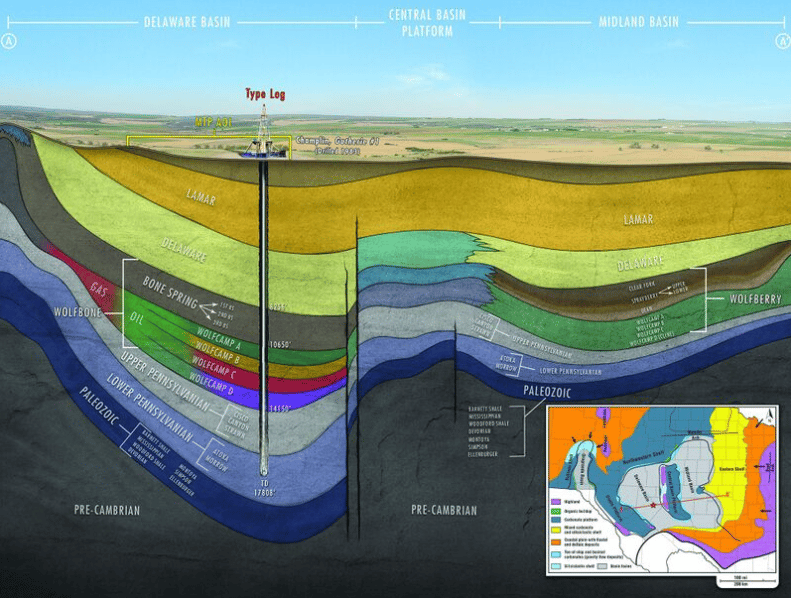

Image directly from https://wiki.seg.org/wiki/Permian_basin. The Wolfberry/Wolfbone sections have been the main Permian development targets for years…is the deeper Paleozoic (Woodford) the next one up?

The Power of Stacked Pay

In the Permian Basin, multiple productive intervals can sit vertically stacked across thousands of feet of rock. Historically, operators focused on the most economic targets first. As technology improved and inventory matured, deeper benches moved into development consideration. For an operator, testing a new bench requires capital. It involves drilling, completion design, infrastructure tie-ins, and execution risk.

For a mineral owner, the equation is different. The mineral interest does not fund drilling. It does not absorb cost overruns. It does not require reinvestment when new zones are tested. Yet it participates in production if and when those zones are developed. That is embedded upside.

Same Acreage, Expanding Opportunity

When stacked pay benches such as the Woodford begin to demonstrate competitive performance, the value of the underlying mineral acreage expands without additional capital from the royalty owner.

The same tract of land can generate revenue from: existing Spraberry or Wolfcamp wells, future Woodford development, potential deeper intervals yet to be fully tested. This layered exposure creates a form of long-term optionality that is difficult to replicate in other asset classes.

Why This Matters Now

As large operators consolidate and refine portfolios, they increasingly focus on extending drilling inventory depth. Deeper benches are part of that strategy.

For royalty investors, that shift can translate into incremental development below already producing intervals. It represents upside driven by evolving geology and technology rather than incremental capital from the investor.

In an industry defined by cycles, that structural asymmetry matters. Optionality without capital risk is not a marketing phrase. It is a structural feature of mineral ownership.

LOOKING AHEAD

From Headlines to Handshakes

This week the industry gathers in Houston for the North American Prospect Expo, better known as NAPE. While media coverage often focuses on the headline mergers and billion dollar transactions, NAPE is where the next phase of those stories begins.

Over the past year, consolidation has reshaped the U.S. shale landscape. Companies such as ExxonMobil, Chevron, SM Energy, Devon Energy, and Ovintiv have expanded positions and refined portfolios. Now we are seeing the second stage of that cycle. Non-core assets are being marketed. Capital is being reallocated. Balance sheets are being reset. NAPE is where those portfolio adjustments move from press release to transaction process.

Behind the scenes, asset packages are reviewed, valuation expectations are tested, and new partnerships are explored. It is often less about dramatic announcements and more about disciplined underwriting. Questions that matter include: Are buyers prioritizing cash flow durability or drilling inventory depth?, Is capital leaning toward oil-weighted positions, natural gas exposure, or stacked pay optionality?, Are valuation spreads narrowing between public sellers and private buyers? These are the conversations that shape the next year of deal flow.

For mineral and royalty investors, this environment is particularly important. When large operators streamline portfolios, assets that may be non-core to a global balance sheet can become core to focused capital. Development can accelerate under new ownership. Cash flow can be optimized through operational attention rather than scale alone.

We view NAPE not simply as a conference, but as a real-time pulse on how disciplined capital is positioning for the next phase of U.S. shale. The tone of the market, the appetite for risk, and the pricing of assets will all provide insight into whether this consolidation cycle is stabilizing or entering its next chapter.

We will be watching closely.

Ways to Connect with Us:

Email: [email protected]

Website: www.petropeakinvest.com

Schedule a Call: Book a time here

Follow us on LinkedIn and socials: PetroPeak Investments LLC, @petropeakinvest

Whether you’re exploring royalties for the first time or looking to deepen your exposure, PetroPeak can guide you through every step from understanding the asset class to participating in high-quality, cash-flowing deals.

Because at PetroPeak, it’s about more than just investing. It’s about building long-term income you can count on.