- PetroPeak Investments Newsletter

- Posts

- Newsletter Feb 3, 2026

Newsletter Feb 3, 2026

John Jordan

February 03, 2026

MARKET PULSE

Shock & Signal: Price Pressure, Freeze-Offs, and Operator Discipline

The last two weeks offered a useful reminder that oil markets can swing on two very different levers at the same time: price-driven capital discipline and unplanned operational disruption. On the price side, a recent Rystad scenario put a sharp stake in the ground: if crude were to slide toward $40/bbl, U.S. shale could decline by as much as ~400,000 bbl/d in 2026, especially if OPEC+ pursues market share over price.

But the counterpoint matters for investors: shale doesn’t “turn off” cleanly on a spot-price headline. The response tends to be delayed and uneven: buffers like hedges, high-grading to top inventory, and cost deflation in the service sector can all slow the initial decline curve. That’s why the real question isn’t “Does lower price reduce activity?” (it does), but how long it takes before activity reductions show up in basin-level volumes and, ultimately, in market balance.

At the same time, weather reminded everyone how quickly non-price factors can tighten the system. Winter Storm Fern knocked meaningful production offline and, even during the recovery, consultancy Energy Aspects estimated U.S. crude output was still down roughly 600,000 bbl/d at one point, with about 250,000 bbl/d of that in the Permian Basin and then improving toward ~500,000 bbl/d still offline shortly after. This is the market’s recurring lesson: even when the longer-term narrative is “plenty of supply,” short, sharp disruptions can create real volatility.

Finally, the corporate tape is reinforcing the same theme: in choppy pricing, the industry leans on scale and efficiency. Devon Energy and Coterra Energy have been reported in advanced merger talks another signal that operators are positioning for durability (inventory depth, cost control, free cash flow, and officially announced 2/2/26). And on the ground, Matador Resources highlighted how execution is still improving in core acreage as large-batch development, longer laterals, and per-well cost reductions exactly the kind of operational momentum that tends to keep development concentrated in the best rock even when sentiment wobbles.

PetroPeak lens: Put together, the market is saying: cycles still happen, but activity increasingly concentrates with the best operators on the best acreage. That backdrop is constructive for a royalty strategy focused on core basins—where development is most likely to persist, and where volatility (from either price or weather) can create upside without taking on operating or capex risk.

Commodity | Current Price ($) | Daily Change |

|---|---|---|

WTI Oil ($) | 62.11 | -0.03 -0.05% |

Henry Hub Gas ($) | 3.25 | +0.01 +0.37% |

Current Rig Count(US lower 48) | Week Change | Year Change |

546 | +2 | -36 |

*Prices are as of 02/02/2026 and sourced from oilprice.com. Rig data is provided by WellDatabase.com and as of 02/02/2026.

ROYALTY SPOTLIGHT

Federal royalties & lease policy — why it still matters (even if you only buy private minerals)

Over the next few weeks, Bureau of Land Management will put another meaningful set of federal acres on the board in Colorado: a March 31, 2026 lease sale covering 90 parcels totaling 52,703 acres, with a formal protest window that runs into early March. On its face, that sounds like a “public-lands” headline—relevant mainly to operators drilling federal minerals. But for royalty investors, it’s better viewed as a forward indicator: federal leasing terms and the appetite to bid (or not bid) can influence where capital concentrates, how quickly regional supply grows, and how durable development programs remain across the cycle.

Here’s the tension worth highlighting. On one hand, the federal government has been pushing to modernize leasing economics and accountability, most notably through higher minimum royalty rates (16.67% minimum for new leases under updated guidance) and reforms around bonding and process. On the other hand, U.S. Department of the Interior has also signaled policy direction that could lower the minimum onshore royalty rate back toward 12.5% (reversing the 16.67% minimum tied to recent reforms), explicitly framing it as a way to stimulate leasing and drilling activity.

So what should your readers watch—not politically, but economically?

In practice, lease sales that attract weak competitive bidding can still result in acreage getting picked up later through noncompetitive leasing at relatively low cost. That matters because it changes the “cost of inventory” for operators in a region. Cheaper inventory (all else equal) can extend drilling runways when prices soften; higher government take or tighter requirements can push capital toward the most advantaged rock and jurisdictions. Either way, policy shapes incentives, and incentives shape where rigs and completion crews ultimately spend their time.

Investor takeaway: We don’t invest in minerals because we expect policy to be perfect—we invest because development capital tends to migrate to the most resilient, repeatable opportunities. Federal leasing headlines help you see that migration early: not just what acres are offered, but who is willing to pay up, and whether activity is likely to concentrate in the best rock (often private) when the cycle turns.

Real Assets. Real Income. Real Alignment. |

BASIN FOCUS

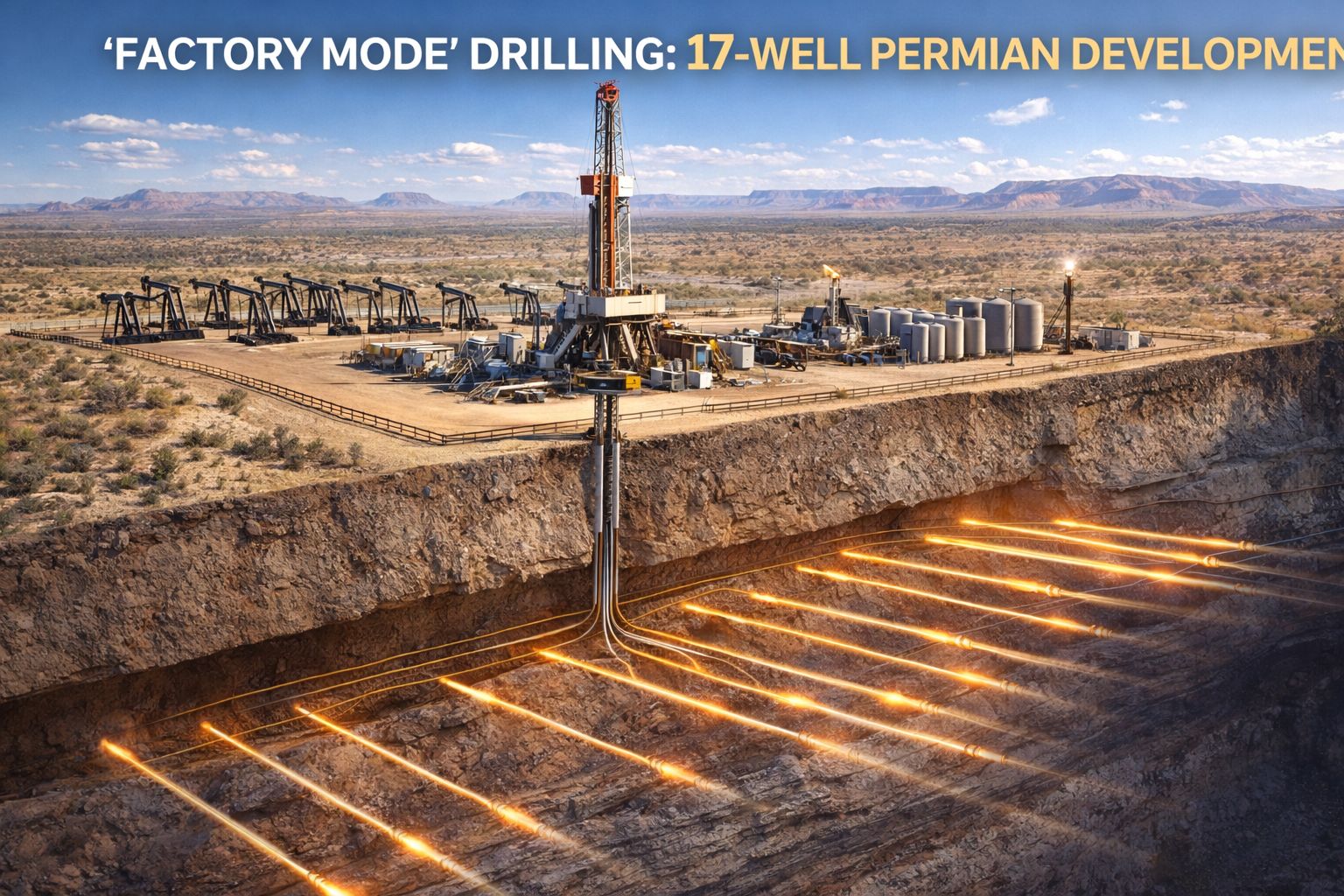

Permian “Factory Mode” is speeding up — and majors are underwriting multi-year growth

The ExxonMobil story in the Permian right now is less about “finding oil” and more about manufacturing repeatable wells at scale. In the Delaware, Exxon has pushed production to 600,000+ boe/d, up about 60% year-over-year, by leaning into cube development (stacked-zone development from a single surface location) and tightening the completion recipe including tests of lightweight proppant that the company says has improved recoveries in some cases.

That “factory mode” theme shows up clearly outside the supermajors, too. Matador Resources highlighted a 17-well batch development in Lea County that delivered production results about 8% above its recent company average, alongside ~10% lower per-well costs helped by longer laterals and multi-well completion approaches (simul/trimul-frac). The common thread: fewer surprises, faster cycles, tighter costs and more predictable development.

The reason this matters for your readers: this isn’t just operational bragging rights. It’s what supports durable growth guidance from the largest balance sheets in the basin. Exxon’s longer-range plan targets a doubling of Permian output by 2030, which is only plausible if the basin keeps operating like a manufacturing system. And Chevron, in its latest quarterly outlook, guided to 7%–10% production growth in 2026 (excluding asset sales), signaling confidence that its growth projects (including U.S. shale contributions) can keep momentum even in a choppy macro tape.

“Factory mode” is what turns a great basin into a repeatable cash-flow engine. When operators can drill in batches, standardize designs, and lower per-well costs, development tends to persist longer through cycles which can translate into more consistent royalty volumes on high-quality acreage in the Delaware Basin.

INVESTOR ADVANTAGE

Volatility upside without operating risk — why gas spikes can help (but don’t have to)

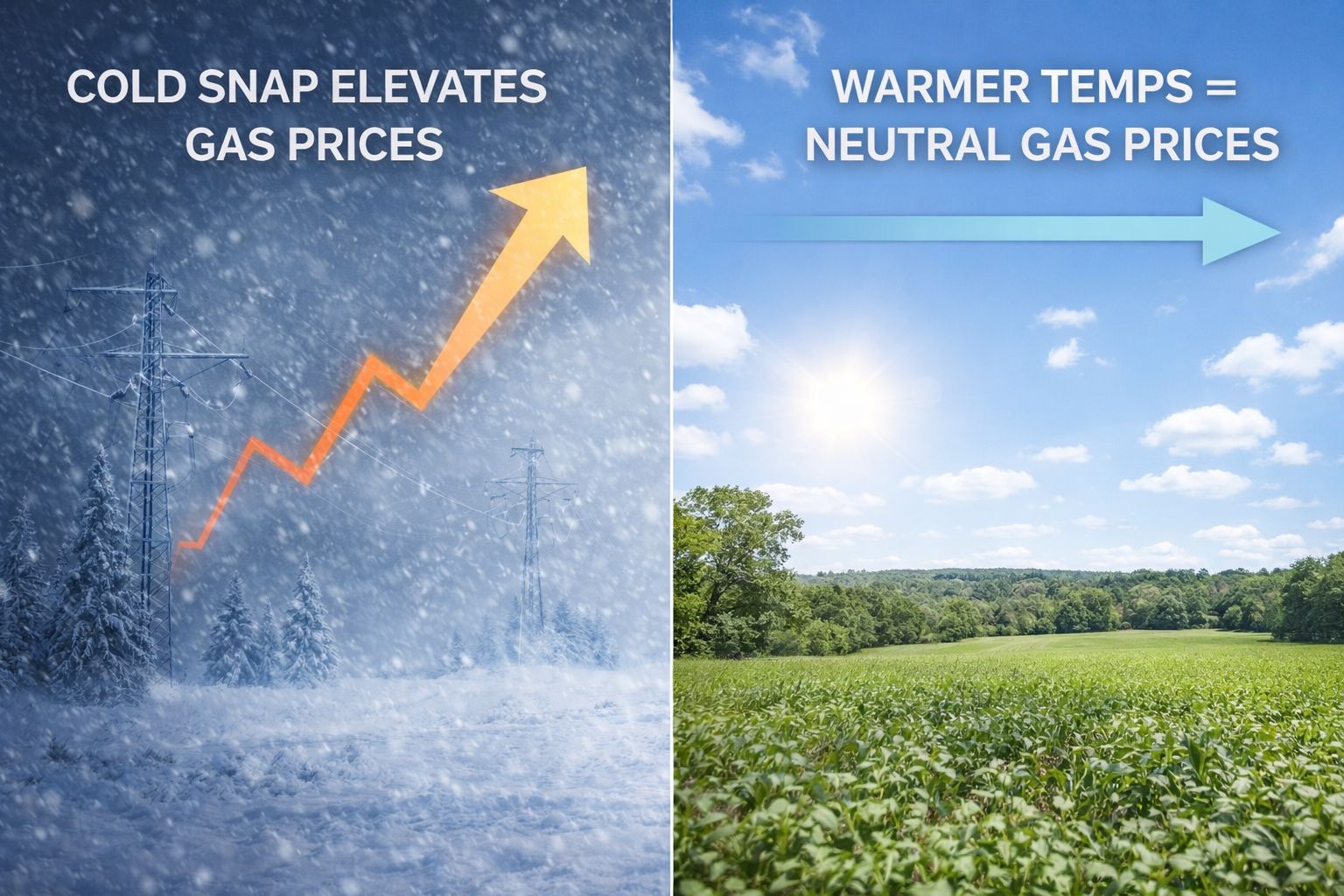

The last two weeks were a live demonstration of something most investors feel but rarely see quantified in real time: when weather + infrastructure constraints + demand line up, energy prices can move fast. Winter Storm Fern triggered widespread freeze-offs and deliverability issues, while heating and power demand surged, driving a sharp rally in the front of the U.S. natural gas market.

For a royalty owner, that kind of dislocation can create “free upside”: you participate in higher realized pricing (where contracts allow), without taking on the operational scramble: no staffing, no winterization logistics, no capex decisions, no downtime risk management. The operator fights the storm; the royalty owner simply owns a share of production revenue.

That said, PetroPeak’s investment thesis doesn’t require price shocks like this. These events are best understood as optional upside. A tailwind when it happens, but not the reason to invest. The core thesis remains: build a portfolio of high-quality minerals/royalties positioned under durable development programs, where cash flow is driven by asset quality and operator activity, not perfect commodity timing.

When does the spike fade? What the market is pricing now

The current consensus across market commentary and the curve is that this was primarily a weather-and-freeze-off-driven premium, not a permanent reset:

The cold was described as intense but shorter-lived, with freeze-offs spiking toward near-record levels on Jan. 25 and then expected to ease as temperatures normalize.

Forecast commentary pointed to the cold wave persisting through late January and into early February (roughly the first week or two of February), which aligns with the idea that the biggest price pressure is front-loaded.

Importantly, longer-dated pricing has not moved nearly as dramatically. The U.S. Energy Information Administration noted that recent futures strength has been concentrated in the near term and hasn’t materially lifted the longer end of the curve, and its broader 2026 view still centers around mid-$3/MMBtu pricing on an annual average basis.

The market is largely treating this as a late-January / early-February event, with the spike expected to subside as freeze-offs reverse and temperatures moderate, rather than a new sustained price regime.

One more timely datapoint to underline the “volatility = optional upside” theme: the gas spike effectively broke yesterday. U.S. Henry Hub futures plunged more than 20% in a single session as forecasts shifted materially warmer for mid-February, pulling prices back toward the low-to-mid $3/MMBtu range that is much closer to the market’s recent baseline than the storm-driven extremes. In other words, the move reinforces the core point for PetroPeak investors: these spikes can be powerful when they happen, but they can also mean-revert quickly, which is why PetroPeak treats price shocks as upside potential, not a required pillar of the investment thesis. For context, the EIA’s current outlook still frames 2026 as a roughly mid-$3/MMBtu year on average (with near-term quarters around that level), which aligns with where prices snapped back today.

Price spikes are a reminder that energy can still behave like an “insurance asset” inside a diversified portfolio, convex in stress, but PetroPeak is built so returns don’t depend on catching storms. When volatility shows up, royalties can benefit; when it doesn’t, the strategy still rests on disciplined acquisition, basin quality, and development durability.

LOOKING AHEAD

Price Signals for 2026: Oil Flat-to-Soft, Gas Supported by Structural Demand

The next 10 days bring a cluster of catalysts that can move near-term pricing and (more importantly) shape operator behavior heading into late winter.

Feb 1: OPEC+ policy check-in: Delegates have signaled the group is likely to extend the current pause on planned production increases into March 2026, even after crude’s recent strength. Watch the tone: “pause” language generally supports price stability; any surprise shift toward market-share would re-ignite downside narratives.

Around Feb 5: Saudi Aramco official selling prices: Reuters reporting suggests March Asia pricing may move to a discount (a notable signal on near-term demand and physical tightness/looseness).

Every Thursday: U.S. Energy Information Administration storage + weather normalization: Natural gas storage releases remain the market’s weekly “truth serum” during winter. Traders will be watching whether withdrawals and freeze-offs normalize after the recent cold-driven dislocation.

Fri Feb 6: Baker Hughes rig count: Rig counts matter less as a weekly trading event than as a trend line, but after the recent volatility they’re a good read on whether operators are leaning into activity or staying disciplined.

Feb 10: EIA Short-Term Energy Outlook (STEO): The next STEO is a key checkpoint for the market’s baseline on U.S. production, demand, and price assumptions heading into spring.

Near-term price moves can be noisy, but these catalysts help reveal behavior: whether capital stays concentrated in “factory mode” basins like the Permian Basin, and whether winter volatility tightens balances long enough to change operator planning. That’s why we treat spikes as optional upside, not a requirement. Our focus remains on high-quality minerals positioned under durable development programs.

Ways to Connect with Us:

Email: [email protected]

Website: www.petropeakinvest.com

Schedule a Call: Book a time here

Follow us on LinkedIn and socials: PetroPeak Investments LLC, @petropeakinvest

Whether you’re exploring royalties for the first time or looking to deepen your exposure, PetroPeak can guide you through every step from understanding the asset class to participating in high-quality, cash-flowing deals.

Because at PetroPeak, it’s about more than just investing. It’s about building long-term income you can count on.