- PetroPeak Investments Newsletter

- Posts

- Newsletter Jan 20, 2026

Newsletter Jan 20, 2026

John Jordan

January 20, 2026

MARKET PULSE

Leasing Appetite Returns as Oil Stays Disciplined and Gas Gains a New Demand Floor

Federal leasing is flashing a clear “risk-on” signal again. On January 6, 2026, the BLM’s quarterly lease sale in New Mexico and Oklahoma generated $326.8 million across 31 parcels (~20,399 acres) including what BLM described as the highest single-acre bid since at least the 1987 Leasing Reform Act. In practical terms: bidders don’t pay record dollars for acreage unless they believe permitting, development timelines, and long-cycle regulatory friction are improving under the current administration.

At the same time, the macro backdrop continues to reinforce an “oil discipline” narrative. The EIA’s Short-Term Energy Outlook expects crude prices to soften in 2026 as global supply outpaces demand and inventories build an environment that typically rewards operators who prioritize returns, efficiency, and balance-sheet strength over volume growth. That dynamic often translates into steadier, more deliberate development programs rather than a boom/bust sprint.

Where the tone is more constructive is natural gas. Demand growth is becoming less “weather-only” and more structural. EIA projects U.S. power consumption to set new records in 2026 and 2027, driven in part by data centers/AI and broader load growth. Meanwhile, U.S. LNG is continuing to scale: 2025 marked the first year a country exported over 100 million metric tons of LNG, and growth is expected to continue as new capacity ramps. Combined, that’s a credible foundation for more bullish running room in gas, even if volatility persists month-to-month.

Why this matters for royalty investors: a more permissive leasing/permitting posture supports sustained development inventory, oil discipline supports more predictable capital allocation, and gas demand tailwinds (power + LNG) can strengthen the cash-flow outlook for gas-weighted minerals without taking on operating or capex risk.

Commodity | Current Price ($) | Daily Change |

|---|---|---|

WTI Oil ($) | 59.43 | +0.09 +0.15% |

Henry Hub Gas ($) | 3.57 | +0.46 +14.93% |

Current Rig Count(US lower 48) | Week Change | Year Change |

546 | -1 | -37 |

*Prices are as of 01/19/2026 and sourced from oilprice.com. Rig data is provided by WellDatabase.com and as of 01/19/2026.

ROYALTY SPOTLIGHT

Development Inventory: The “Hidden Asset” Behind Long-Term Royalty Upside

Most investors discover mineral royalties through the cash flow. The idea is intuitive: wells produce, revenue is generated, and a royalty owner receives a share without paying for drilling, lifting costs, or day-to-day operations. That current income matters, and it’s often the first thing people look at when evaluating an opportunity.

But the long-term durability of a royalty position usually comes from something quieter and often far more valuable: development inventory.

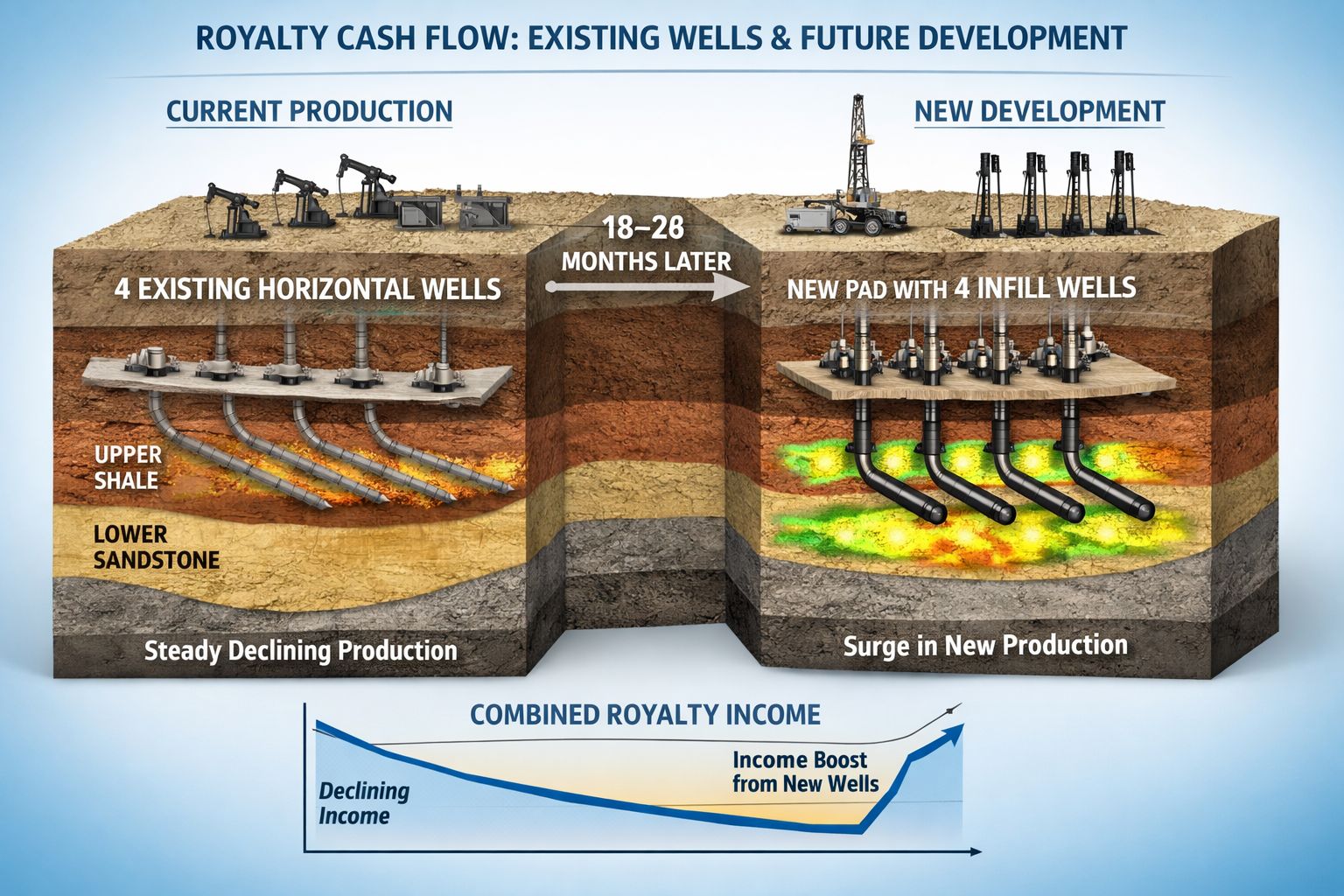

Development inventory is the operator’s runway. It’s the set of future wells that could be drilled across the acreage where your minerals sit. In many ways, it’s the difference between owning a royalty that simply declines over time and owning a royalty position with embedded optionality where new wells can refresh production, extend the life of the asset, and create additional upside without requiring additional capital from you.

The simplest way to think about it is this: existing wells are today’s rent. Development inventory is the property’s ability to add units over time.

Every producing well declines. That isn’t a risk unique to royalties it’s the physics of reservoirs. So the question becomes: what happens after the initial production base starts to taper? In the best royalty positions, the answer is straightforward: new wells arrive, typically as part of repeatable, manufacturing-style development. Those new wells can offset decline from older wells and help maintain a more durable income stream over a multi-year period.

This is why “inventory” is not just an operator buzzword. It’s a tangible driver of future cash flow if it’s real. The best inventory shows up in the field, not in a slide deck. It’s visible in multi-pad development, repeated well results, and a pattern of execution that continues through commodity cycles. When operators are disciplined, they may slow overall drilling but they tend to keep investing in their strongest assets. High-quality rock with deep runway is more likely to stay in the program than fringe acreage that only works in boom times.

Inventory also matters because it creates optionality without adding operating risk. As a mineral owner, you don’t have to decide when to deploy drilling capital. You don’t have to approve budgets. You don’t have to fund cost overruns. Operators will drill when economics justify it based on price, service costs, infrastructure constraints, and corporate strategy. If your minerals sit in the right place, you participate when the operator exercises that option. In effect, inventory can provide upside exposure that remains “on the shelf” until the market conditions are favorable without you having to write another check.

And when development comes, it often doesn’t arrive gradually. A new pad can create a step-change in production near or on your acreage, which can translate into a noticeable increase in royalty revenue. That’s one reason we underwrite beyond “what’s producing today.” We care about current cash flow, but we also evaluate the runway behind it: the geology, the operator’s demonstrated activity, the presence of infrastructure, and the economic resilience of the asset at mid-cycle prices.

So when we say we focus on quality minerals, we’re not only talking about what the asset is paying now. We’re talking about whether it has the potential to remain relevant whether it sits inside repeatable development corridors where future wells are likely to be drilled, not just theoretically possible.

Investor takeaway: Royalty investing isn’t only about owning cash flow. It’s about owning cash flow plus runway. Development inventory is the runway and when it’s real, it can turn a royalty position from a declining stream into an asset with more durable income and embedded upside over time.

Real Assets. Real Income. Real Alignment. |

BASIN FOCUS

DJ Basin (Wattenberg): Repeatable Inventory, Repeatable Cash Flow

If you’ve followed PetroPeak for any length of time, you’ve heard me speak positively about the DJ Basin, and for good reason. The basin has quietly become one of the most repeatable places in the Lower 48 to turn development inventory into durable production, especially in the core Wattenberg fairway. What makes the DJ stand out for royalty owners isn’t hype or headline-grabbing growth; it’s the way the basin lends itself to manufacturing-style development: pad drilling, predictable rock, and projects that can be executed efficiently.

A recent proof point comes from Civitas Resources, one of the basin’s flagship operators. In its latest reported operating update, Civitas highlighted results from its Invicta development in Watkins, where the project surpassed ~1 million BOE after 105 days (approximately 80% oil) and included eight long-lateral wells that exceeded performance expectations. Civitas also noted a company drilling record running a two-mile lateral to total depth in ~1.3 days (excluding surface drilling) a good indicator of execution efficiency that matters when capital is disciplined and schedules matter.

Zooming out, Civitas reported the DJ’s operational momentum in the same update: DJ Basin production increased ~6% quarter-over-quarter to ~155 MBoed, with oil volumes up ~9% to ~72 MBbl/d, even while the company navigated portfolio changes.

Why this matters for PetroPeak investors: the DJ is a basin where development inventory tends to translate into real wells on real schedules. When an operator like Civitas executes multi-well pads with strong early-time performance, it illustrates the “inventory refresh” concept we covered in Royalty Spotlight: legacy wells decline, but new pads can create step-changes in production that help sustain (or lift) royalty cash flow without the royalty owner taking on drilling cost or operational risk.

INVESTOR ADVANTAGE

Runway Without Reinvestment Built for a Discipline-First Market

One of the most overlooked benefits of mineral royalties is that they can combine durable cash flow today with embedded upside tomorrow without asking investors to keep funding the business along the way.

That matters even more in today’s “discipline-first” oil market. Public operators are being rewarded for free cash flow, returns, and balance-sheet strength, not aggressive production growth. In practical terms, that often means drilling programs are planned with more care: fewer speculative steps, more repeatable development, and a stronger emphasis on executing the best inventory efficiently.

For royalty investors, that environment can be a feature, not a bug. Royalties are positioned to participate in development when operators choose to drill, but royalty owners are not asked to share in the costs or the operational volatility that comes with that decision. There are no capital calls, no exposure to LOE overruns, and no requirement to “reinvest” just to keep the asset producing.

This is where development inventory becomes the advantage. As legacy wells naturally decline, follow-on pads and infill development can “refresh” the production base often creating a stair-step pattern in cash flow over time. The operator supplies the capital and execution; the royalty owner participates in the resulting production and revenue.

In a market where operators are optimizing for returns and pacing development accordingly, mineral royalties offer a rare combination of runway without reinvestment, and cash-flow exposure that can remain resilient even when capital discipline is the rule.

LOOKING AHEAD

Price Signals for 2026: Oil Flat-to-Soft, Gas Supported by Structural Demand

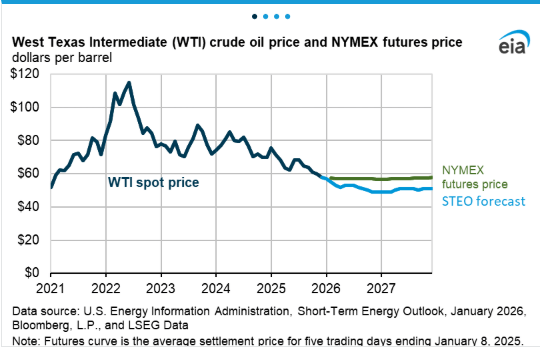

Looking into 2026, the EIA’s latest Short-Term Energy Outlook (January edition) frames a familiar setup for crude: global supply growth is expected to outpace demand, driving continued inventory builds and keeping prices flat to slightly depressed. In EIA’s base case, Brent averages about $56/bbl in 2026 (down from ~$69/bbl in 2025), with the pressure easing only gradually as inventory builds moderate later in the forecast.

Natural gas has a different set of tailwinds. While EIA’s annual average Henry Hub forecast for 2026 is roughly $3.46/MMBtu (near-flat versus 2025), the supportive signal is why the market tightens later: LNG exports continue to grow and power-sector gas burn rises as U.S. electricity demand expands, including load growth tied to data centers. EIA also expects new LNG capacity to begin operating during 2026, which helps underpin demand as the year progresses.

This is a “discipline tape” for oil where returns and efficiency matter most while gas has a more constructive medium-term backdrop as exports and power demand keep pushing the demand floor higher, even if month-to-month volatility persists.

Ways to Connect with Us:

Email: [email protected]

Website: www.petropeakinvest.com

Schedule a Call: Book a time here

Follow us on LinkedIn and socials: PetroPeak Investments LLC, @petropeakinvest

Whether you’re exploring royalties for the first time or looking to deepen your exposure, PetroPeak can guide you through every step from understanding the asset class to participating in high-quality, cash-flowing deals.

Because at PetroPeak, it’s about more than just investing. It’s about building long-term income you can count on.