- PetroPeak Investments Newsletter

- Posts

- Newsletter March 17, 2026

Newsletter March 17, 2026

John Jordan

March 17, 2026

MARKET PULSE

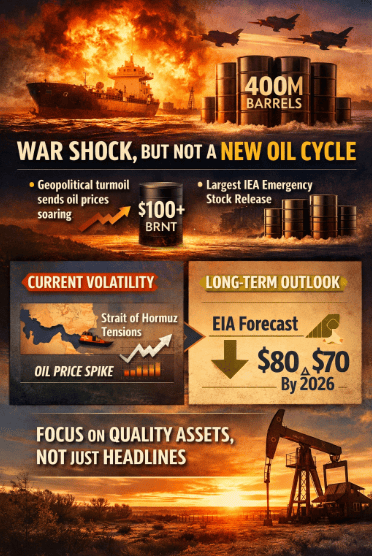

War Shock, But Not a New Oil Cycle

Oil prices surged over the past two weeks as conflict involving Iran and disruption risk around the Strait of Hormuz pushed Brent back above $100 per barrel. The move was sharp, but the bigger question for investors is whether this marks the start of a durable new oil cycle or simply a temporary geopolitical shock.

The immediate reaction is understandable. Roughly one-fifth of global oil trade normally moves through the Strait of Hormuz, so even a short-lived disruption can trigger a violent repricing in crude. That risk became serious enough for the International Energy Agency to coordinate the largest emergency oil stock release in its history, with member countries agreeing to make 400 million barrels available to the market.

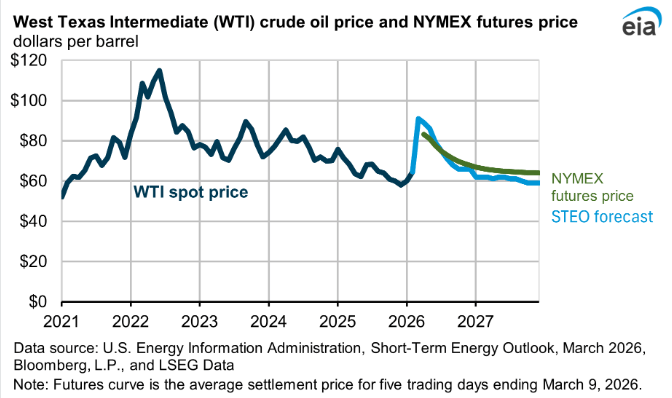

But while the shock is real, it does not automatically mean the market has entered a lasting higher-price regime. The U.S. Energy Information Administration said in its March Short-Term Energy Outlook that Brent is expected to remain above $95 per barrel in the near term, then fall below $80 in the third quarter of 2026 and trend toward $70 by year-end, assuming disruptions begin to ease. For royalty-focused investors, that distinction matters. Near-term price spikes can improve sentiment and support cash flow expectations, but long-term value is still created by owning quality minerals in active basins with strong operators and repeatable economics. In our view, this is a market shock worth respecting but not yet proof of a permanently higher oil cycle. |  |

Commodity | Current Price ($) | Daily Change |

|---|---|---|

WTI Oil ($) | 96.01 | +2.51+2.68% |

Henry Hub Gas ($) | 3.03 | +0.01+0.10% |

Current Rig Count(US lower 48) | Week Change | Year Change |

553 | +2 | -39 |

*Prices are as of 03/16/2026 and sourced from oilprice.com. Rig data is provided by WellDatabase.com and as of 03/16/2026.

ROYALTY SPOTLIGHT

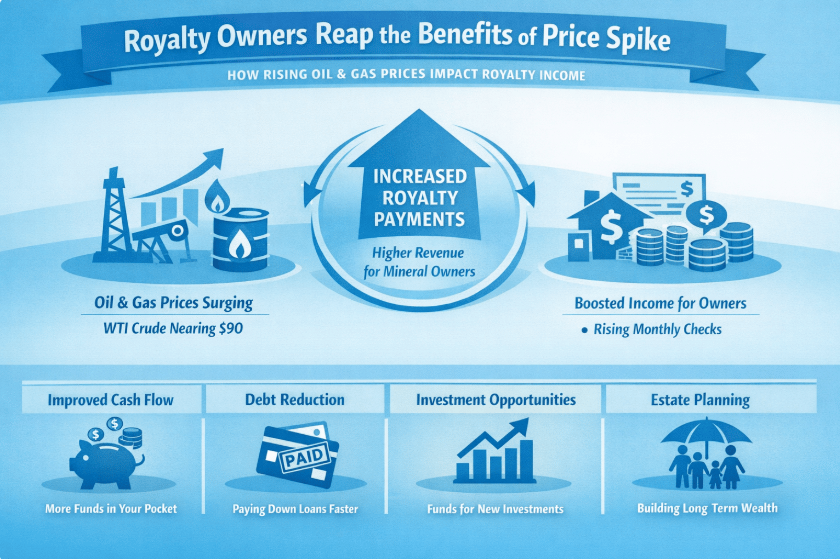

What a Price Spike Actually Means for Royalty Owners

Oil prices moved sharply higher over the past two weeks as conflict involving Iran and disruption risk around the Strait of Hormuz pushed Brent above $100 per barrel, with intraday highs briefly reaching nearly $120 before pulling back.

For royalty owners, that kind of move matters but not always in the way headlines suggest. A higher oil price can support stronger royalty revenue, yet the impact is rarely immediate, linear, or permanent. Royalty income still depends on several moving parts: actual production volumes, product mix, realized pricing, transportation and marketing terms, and the timing of when barrels are sold and reported. A sudden spike in crude may lift sentiment quickly, but it does not automatically create a lasting step-change in monthly royalty checks. This is especially true if the price move is driven by temporary geopolitical fear rather than a long-term shift in supply and demand.

That distinction is especially important right now. The International Energy Agency announced that member countries would make 400 million barrels available from emergency reserves in response to the market disruption, while the EIA’s March outlook still projects Brent to remain above $95 per barrel near term before falling below $80 in the third quarter of 2026 and to around $70 by year-end. In other words, the market is recognizing the seriousness of the shock, but official forecasts still point to moderation once supply disruptions begin to ease.

For mineral investors, the takeaway is straightforward: short-term oil spikes can be beneficial, but long-term royalty value is still built on quality acreage, strong operators, and repeatable development activity. Price matters, but durable cash flow comes from owning assets that continue to be developed through multiple market cycles not just during headline-driven surges.

Real Assets. Real Income. Real Alignment. |

BASIN FOCUS

Why Strong Operators Matter More Than Short-Term Headlines

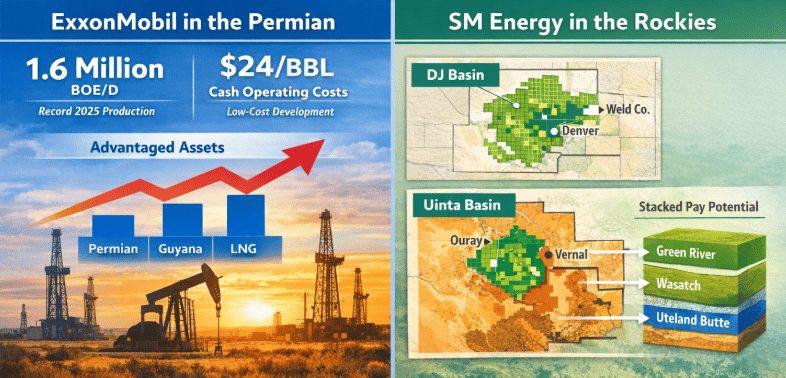

In volatile commodity markets, basin quality is only part of the story. The other part is operator quality. Recent results from ExxonMobil and SM Energy are a good reminder that the most durable royalty value is often created not by a short-lived price spike, but by strong operators deploying capital in their best rock with discipline and scale.

In the Permian, ExxonMobil continues to reinforce why the basin remains the premier U.S. oil development engine. The company reported that full-year 2025 production reached its highest level in more than 40 years, with Permian output averaging 1.6 million oil-equivalent barrels per day for the year. Exxon also identified the Permian as part of its core “advantaged assets” base, alongside Guyana and LNG, underscoring that the basin remains central to its long-run growth strategy rather than just a short-term response to commodity prices.

That matters for royalty owners because large, well-capitalized operators tend to keep moving through the cycle. When a company like Exxon is building around low-cost, scalable inventory, the basin benefits from more consistent development, more repeatable well results, and a stronger foundation for long-term royalty cash flow. In that sense, the Permian story is not simply about high oil prices. It is about sustained capital commitment from an operator with the balance sheet and inventory depth to keep developing through changing market conditions.

A similar message is emerging from SM Energy in the DJ and Uinta. In its 2026 outlook, SM described its portfolio as an “expanded, top-tier asset portfolio” and emphasized capital efficiency, free cash flow, and inventory value. The company’s current plan allocates roughly 20% of capital to the DJ and another 20% to the Uinta, with about 80 net wells expected online in the DJ and about 30 in the Uinta during 2026. That is a meaningful signal that these basins are not side bets, they are core development areas competing for capital on returns.

For mineral and royalty investors, that is the real takeaway this week. The best royalty assets are not just located in good basins; they are backed by operators with the scale, capital discipline, and development inventory to keep drilling when headlines turn noisy. Exxon’s Permian position and SM’s focused push in the DJ and Uinta show why strong operators can matter more than short-term market swings. Over time, that operating strength is what helps convert quality acreage into durable royalty value.

INVESTOR ADVANTAGE

Why U.S. Energy Exposure Can Be a Useful Diversifier in a Geopolitically Unstable World

The past two weeks have been a reminder that energy markets do not move in isolation. As conflict in the Middle East escalated and tanker traffic through the Strait of Hormuz was disrupted, oil prices surged and governments moved quickly to stabilize supply. Roughly 20% of the world’s oil typically moves through Hormuz, which is why even a regional conflict can have immediate global market consequences.

For investors, that matters beyond the price of gasoline. It highlights why U.S. energy exposure can play a useful role inside a broader portfolio. Domestic mineral and royalty assets are tied to real producing properties in a sector that often responds differently than traditional equities when geopolitical risk rises. While many paper assets can sell off on uncertainty, energy-linked assets may benefit when supply security becomes more valuable. That does not make them immune to volatility, but it does make them a potentially useful diversifier in a world where geopolitical shocks can quickly ripple through financial markets. This is an inference based on how energy markets respond to physical supply disruptions and how domestic production can gain relative importance when global trade routes are stressed.

That same dynamic is visible in the official market response. On March 11, the IEA announced its largest-ever collective oil stock release, making 400 million barrels available to the market in response to disruptions from the Middle East conflict. At the same time, the EIA said it expects Brent crude to remain above $95 per barrel over the next two months before easing later in 2026 if disruptions begin to fade. In other words, the near-term shock is real, but so is the longer-term need for stable, reliable supply.

For PetroPeak’s model, the takeaway is straightforward: mineral royalty ownership offers investors exposure to domestic energy production without taking on operating risk. In periods of geopolitical instability, that combination of hard-asset backing, U.S. production exposure, and potential income generation can offer a form of diversification that is difficult to replicate in more conventional parts of the market. This is not about chasing headlines. It is about owning assets that can remain relevant when global energy security moves back to the center of the investment conversation.

LOOKING AHEAD

Energy Security Is Back at the Center of the Investment Conversation

The last two weeks have been a sharp reminder that energy security can move from background concern to front-page issue very quickly. The Strait of Hormuz remains one of the world’s most critical energy chokepoints, and the recent Middle East conflict was serious enough for the International Energy Agency to announce the largest emergency oil stock release in its history, making 400 million barrels available to the market.

That response matters because it reinforces a broader point: reliable supply still matters. Even in a market shaped by technology, financial flows, and short-term sentiment, the global economy still depends on real barrels, real infrastructure, and dependable production. The IEA said oil from emergency reserves will soon begin flowing to global markets, underscoring how central physical supply security remains when disruption hits.

At the same time, current forecasts suggest this shock may not define the entire year. The EIA expects Brent crude to stay above $95 per barrel over the next two months, then fall below $80 in the third quarter of 2026 and to around $70 by year-end, assuming disruptions begin to ease. The agency also expects U.S. crude oil production to average 13.6 million barrels per day in 2026 and 13.8 million in 2027.

For investors, that creates an important backdrop for the months ahead. Energy security is likely to remain a central theme even if oil prices retreat from recent highs. In our view, that should continue to support attention on U.S. resource basins, strong operators, and royalty assets tied to domestic production. The immediate shock may fade, but the market’s renewed focus on secure, dependable supply could last much longer. This final point is an inference based on the IEA’s emergency response and the EIA’s outlook for continued U.S. production strength.

Ways to Connect with Us:

Email: [email protected]

Website: www.petropeakinvest.com

Schedule a Call: Book a time here

Follow us on LinkedIn and socials: PetroPeak Investments LLC, @petropeakinvest

Whether you’re exploring royalties for the first time or looking to deepen your exposure, PetroPeak can guide you through every step from understanding the asset class to participating in high-quality, cash-flowing deals.

Because at PetroPeak, it’s about more than just investing. It’s about building long-term income you can count on.