- PetroPeak Investments Newsletter

- Posts

- Newsletter March 3, 2026

Newsletter March 3, 2026

John Jordan

March 03, 2026

MARKET PULSE

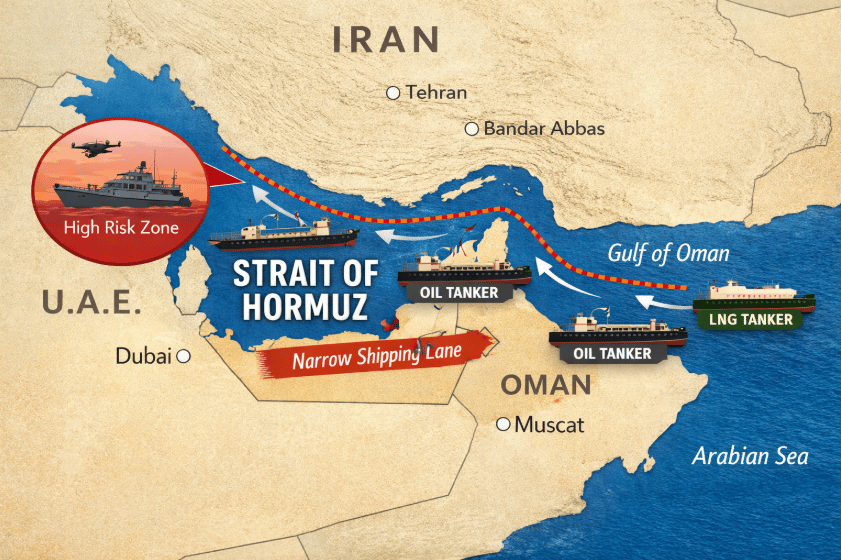

It’s not just barrels: shipping risk is the real price shock

Oil’s latest jump isn’t being driven by a sudden shortage of crude in the ground, it’s a logistics shock. As the Iran conflict escalates, the market is repricing the ability to move molecules, not merely headline supply. The Strait of Hormuz is the key: it’s a narrow chokepoint that handles roughly ~one-fifth of global oil trade and a meaningful share of LNG flows, so even a “de facto” disruption forces traders to price in worst-case outcomes fast.

When tankers can’t transit normally, or can only transit at sharply higher cost, global crude becomes “stranded,” and refiners/importers bid up alternatives. That’s why you can see a price shock even if OPEC+ signals modest output increases: additional supply doesn’t help much if the main constraint is safe delivery.

What’s changing beneath the headlines

Marine insurers are pulling back. Major clubs are reportedly canceling war-risk coverage for Gulf transits (or repricing it dramatically), which immediately raises delivered costs and reduces available vessels willing to run the route. Reuters reported war-risk premiums rising up to ~1% of ship value in some cases real money that cascades into freight rates and netbacks.

Shipping is backing up. Reuters also cited roughly ~150 ships stranded around the Strait amid attacks/damage to vessels, another way a “flow problem” becomes a “price problem.”

Small OPEC+ adds don’t offset chokepoint risk. Output tweaks are incremental; Hormuz disruption is binary. Traders will focus on shipping flows and threat levels, not press-release barrels.

What to watch next that could move prices

Transit normalization

Insurance availability and premiums

Any escalation impacting regional facilities

Forward curve reaction: whether the market prices this as a short spike or a sustained risk regime. Citi flagged Brent could trade ~$80–$90 near-term absent de-escalation, with potential pullback if tensions ease.

PetroPeak investor royalty-relevant takeaway

Royalties can benefit disproportionately in moments like this because the upside can come from price and realizations rather than operators needing to “spend more to earn more.” In other words: geopolitical risk can lift commodity pricing even when U.S. activity remains disciplined, which tends to support near-term cash flow across diversified mineral positions.

Commodity | Current Price ($) | Daily Change |

|---|---|---|

WTI Oil ($) | 71.36 | +4.34 +16.48% |

Henry Hub Gas ($) | 2.93 | +0.12 +4.34 |

Current Rig Count(US lower 48) | Week Change | Year Change |

550 | -1 | -43 |

*Prices are as of 03/02/2026 and sourced from oilprice.com. Rig data is provided by WellDatabase.com and as of 03/02/2026.

ROYALTY SPOTLIGHT

The Title Stack: Why Royalty Due Diligence Is the Real “Edge”

If mineral royalties were as simple as buying a stock, everyone would do it. The reality is that most of the value in royalty investing is created before the first check ever arrives by proving what you actually own, what you’re entitled to be paid, and whether anything in the chain of ownership can interrupt that payment. That’s the title stack.

A “title stack” is simply the full set of documents that establish and define ownership through time: deeds, probate filings, conveyances, leases, assignments, reservations, and amendments. In the royalty world, it’s not uncommon for an asset to have decades of transfers, and the economics can change quietly along the way. That’s why two “similar-looking” mineral packages can produce very different cash flow outcomes.

Why title is different in royalties (and why it creates opportunity)

Unlike many traditional investments, royalties are tied to real property rights. Those rights are frequently split, reserved, inherited, and partially conveyed across generations. The result is an investment category that’s still structurally inefficient and in a market like that, rigorous diligence becomes a competitive advantage.

Five title and diligence pitfalls that matter to investors

Here are five of the most common issues that separate a clean royalty purchase from a future headache:

Chain-of-title gaps: A missing deed, mis-indexed document, or incomplete transfer can break the ownership trail. If ownership isn’t clearly proven, revenue can end up in suspense until cured.

Probate and heirship issues Mineral ownership frequently passes through estates. If probate was never completed (or was done incorrectly), ownership can remain legally uncertain. This is one of the most common reasons operators hold revenue until documentation is corrected.

NPRI/ORRI burdens you didn’t price correctly: Non-participating royalty interests (NPRI) and overriding royalty interests (ORRI) can sit “on top” of a lease. If these burdens exist, the net revenue interest (NRI) available to the mineral owner can be materially lower than expected sometimes without being obvious in a marketing package.

Lease terms that quietly change the economics Royalty rate is only part of the story. Lease clauses can shift value through:

Post-production deductions, Depth/formation limitations, Pugh clauses (or lack of them), Shut-in provisions, Two leases with the same royalty rate can deliver different realized cash flows.

Decimal errors and pay deck mismatches: Even when title is clean, operator payment systems can carry forward old decimals or interpret documents incorrectly. Catching and correcting a small decimal issue can materially change long-term economics.

PetroPeak takeaway: diligence is the moat

This is why we treat the title stack as a core underwriting input, not a back-office formality. In our process, we’re not just buying “mineral acres”, we’re buying verified net revenue interest with a clear line of sight to cash flow.

That diligence discipline tends to do two things for investors:

Reduces downside surprises (suspense, curative costs, delayed payments)

Creates mispricing opportunity where sellers don’t fully understand the title-driven economics

In a world where operators have gotten more efficient and drilling has become “factory mode,” title diligence remains one of the few places where careful work can still create an edge because it’s hard, specialized, and easy to skip.

Real Assets. Real Income. Real Alignment. |

BASIN FOCUS

2026 Playbook: Capital Discipline + Shareholder Returns (Permian & broader U.S. shale)

Across this past week’s earnings releases, the message from large-cap and Permian-weighted operators has been remarkably consistent: 2026 is shaping up as a “durable cash-flow” year, built on measured activity levels, tighter capital programs, and a clear priority on dividends and buybacks over chasing growth. For mineral and royalty owners, that combination matters because it tends to support steady development cadence (the engine for long-lived royalty cash flow) while keeping operators focused on high-quality inventory and execution, the exact conditions where royalties can compound quietly.

The common thread: “steady barrels, better cash”

Several of the companies you flagged are explicitly mapping 2026 around flat-to-moderate production targets and free cash flow conversion, with shareholder returns framed as a core output, not an afterthought.

Occidental (OXY): OXY’s 4Q25 update highlighted continued balance-sheet repair and an 8% dividend increase, alongside a 2026 plan that emphasizes disciplined spending and cash generation.

Diamondback (FANG): Diamondback’s outlook points to stable oil production with a defined 2026 capex range and continued return-of-capital focus (dividends + repurchases).

Ovintiv (OVV): Ovintiv’s release is one of the clearest statements of the “returns-first” mindset: a 2026 program sized to deliver volumes while targeting at least 75% of free cash flow returned to shareholders via dividend + buybacks.

EOG: EOG guided 2026 production and capex while tying the plan to a specific free-cash-flow goal and an ongoing shareholder return framework.

ConocoPhillips (COP): COP reiterated 2026 capex guidance and return-of-capital priorities, and continues to actively high-grade the portfolio through asset sales/dispositions as a reminder that “discipline” includes constantly reshaping the basin footprint.

What this means for the Development Plans (and for royalties)

1) The “factory” doesn’t need more rigs to keep paying. In basins like the Permian (and to a lesser extent the DJ), a lot of value comes from repeatability: pad development, faster cycle times, and incremental cost improvements. When companies size 2026 around “returns + resilience,” they typically keep development focused on core benches and proven designs, which can translate into more predictable royalty cash flows than boom/bust drilling sprees.

2) Capital discipline often concentrates activity in the best rock. When the market rewards buybacks/dividends, operators are incentivized to drill only the highest-return locations. For royalty owners, that can be a feature: better wells, better payout, and fewer “science projects.”

3) Portfolio high-grading can create mineral opportunity. As COP’s reported portfolio streamlining shows, large operators may sell non-core positions even inside major basins. That can shift operatorship, change development sequencing, or open the door for mineral buyers to acquire in areas where public E&Ps are rotating capital.

Simple indicators that tell you if the playbook is holding

Capex vs. activity reality: Are companies actually holding programs flat as guided or quietly adding crews mid-year?

Completion intensity: Even if rigs stay flat, completions can rise (or fall), which directly drives royalty cash flow timing.

Return-of-capital durability: Dividends are “sticky”; buybacks are flexible. Watch language around buyback pacing if prices soften.

The market’s current reward system, discipline, inventory quality, and shareholder returns, is generally constructive for well-positioned mineral owners. It supports a base case of steady development in core areas with fewer value-destructive growth swings. That’s the kind of environment where a diversified royalty portfolio can do what it’s built to do: turn operational execution into durable cash flow.

INVESTOR ADVANTAGE

Return-of-Capital vs. Return-on-Capital

Public E&Ps are starting to look a lot more like mature cash businesses. This past week’s earnings releases reinforced a theme we’ve been watching for several quarters: operators are sizing 2026 plans around capital discipline, efficiency, and returning cash to shareholders, not chasing growth for growth’s sake. That’s a constructive backdrop for energy investors, but it also raises a useful portfolio question: do you want your energy returns to depend on corporate decisions and stock-market multiples, or on production cash flow itself?

On the equity side, the return story is real. Companies are explicitly framing dividends and buybacks as a primary output of the business. EOG, for example, emphasized that it generated meaningful free cash flow and returned it to shareholders through dividends and repurchases, including a dividend increase continuing the “cash first” playbook into 2026. Ovintiv made the message even more explicit, targeting at least 75% of full-year free cash flow returned to shareholders via dividends and buybacks. Occidental also highlighted an increased dividend and balance-sheet priorities alongside its forward plan. ConocoPhillips paired its 2026 guidance with continued emphasis on disciplined capital and shareholder returns another signal that this approach is now the base case for major operators.

But even in a disciplined cycle, equity returns still carry layers that are unrelated to how wells perform. Buybacks can be timed well, or poorly. Capital allocation can shift toward acquisitions, divestitures, or new projects. And market multiples can compress even when execution is strong. In other words, return-of-capital may be consistent, but it’s still a corporate choice, filtered through management decisions and stock market sentiment.

That’s where mineral and royalty ownership fits differently in a portfolio. Royalties are not dependent on a board deciding how much cash comes back through buybacks or dividend policy. They’re tied more directly to what’s happening at the well and basin level: production volumes, realized commodity prices, and the lease terms that define net revenue interest. When the industry is running a “discipline + returns” playbook, royalties can still participate in the same high-quality development that supports free cash flow without requiring investors to underwrite buyback pacing, valuation multiples, or changes in corporate strategy.

The simplest way to describe the difference is this: owning an E&P stock means trusting a company to convert its resource base into shareholder value; owning royalties means participating in revenue from the resource as it’s produced. In today’s environment where operators are focused on repeatable development and cash generation royalties can be a useful complement to E&P equities, aiming to capture energy cash flow drivers while reducing exposure to equity-market noise.

LOOKING AHEAD

Shock vs. Signal: What the Iran “price premium” means for 2026

This week’s newsletter has one clear through-line: markets can spike on headlines, but portfolios compound on fundamentals. The Iran conflict has injected a real risk premium into oil, driven less by geology and more by shipping security, insurance, and chokepoint logistics, and that can move prices quickly even when underlying supply/demand hasn’t changed overnight.

At the same time, the “signal” coming from corporate earnings is remarkably steady. Across major operators, 2026 planning is still anchored to capital discipline, efficiency, and returning cash to shareholders rather than chasing high-growth production targets. That matters for royalties because disciplined programs tend to concentrate activity in core inventory and sustain a predictable development cadence the quiet engine behind durable royalty cash flow.

So how do we reconcile a war-driven price shock with a “disciplined 2026” corporate playbook?

The EIA baseline (pre-shock): softer prices and slower growth in 2026

Before this latest escalation, the EIA’s base case already leaned bearish for 2026: global inventories building as production growth outpaces demand growth, pulling prices lower over time. In its February 2026 Short-Term Energy Outlook, the EIA forecast Brent averaging about $58/bbl in 2026 (and lower again in 2027), with the core driver being persistent stock builds.

On the U.S. side, EIA also expects crude production growth to slow in 2026 as operators respond to lower prices and prioritize “value per barrel” over volume consistent with what management teams are communicating in earnings.

The “war premium”: near-term upside, but it must fight the inventory math

Geopolitical risk can absolutely keep prices elevated in the near term especially if shipping flows tighten or war-risk premiums rise. But unless disruptions become sustained and material, the market tends to revert back toward the bigger forces: inventory direction, demand growth, and non-OPEC supply response. That’s why the EIA can simultaneously acknowledge short-term disruptions while still forecasting lower average prices through 2026 in its baseline outlook.

In environments like this, it’s helpful to separate short-term pricing shocks from multi-quarter fundamentals. The news can move oil fast, but the longer arc of 2026 still looks like a contest between (a) a geopolitics-driven premium and (b) the EIA’s pre-shock baseline of inventory builds and softer average pricing.

For royalty investors, that’s precisely why disciplined operator behavior and high-quality basin exposure matter: you want assets that can perform across both regimes capturing upside when prices surprise higher, while remaining resilient when the market re-anchors to fundamentals.

Ways to Connect with Us:

Email: [email protected]

Website: www.petropeakinvest.com

Schedule a Call: Book a time here

Follow us on LinkedIn and socials: PetroPeak Investments LLC, @petropeakinvest

Whether you’re exploring royalties for the first time or looking to deepen your exposure, PetroPeak can guide you through every step from understanding the asset class to participating in high-quality, cash-flowing deals.

Because at PetroPeak, it’s about more than just investing. It’s about building long-term income you can count on.