- PetroPeak Investments Newsletter

- Posts

- Newsletter March 31, 2026

Newsletter March 31, 2026

John Jordan

March 31, 2026

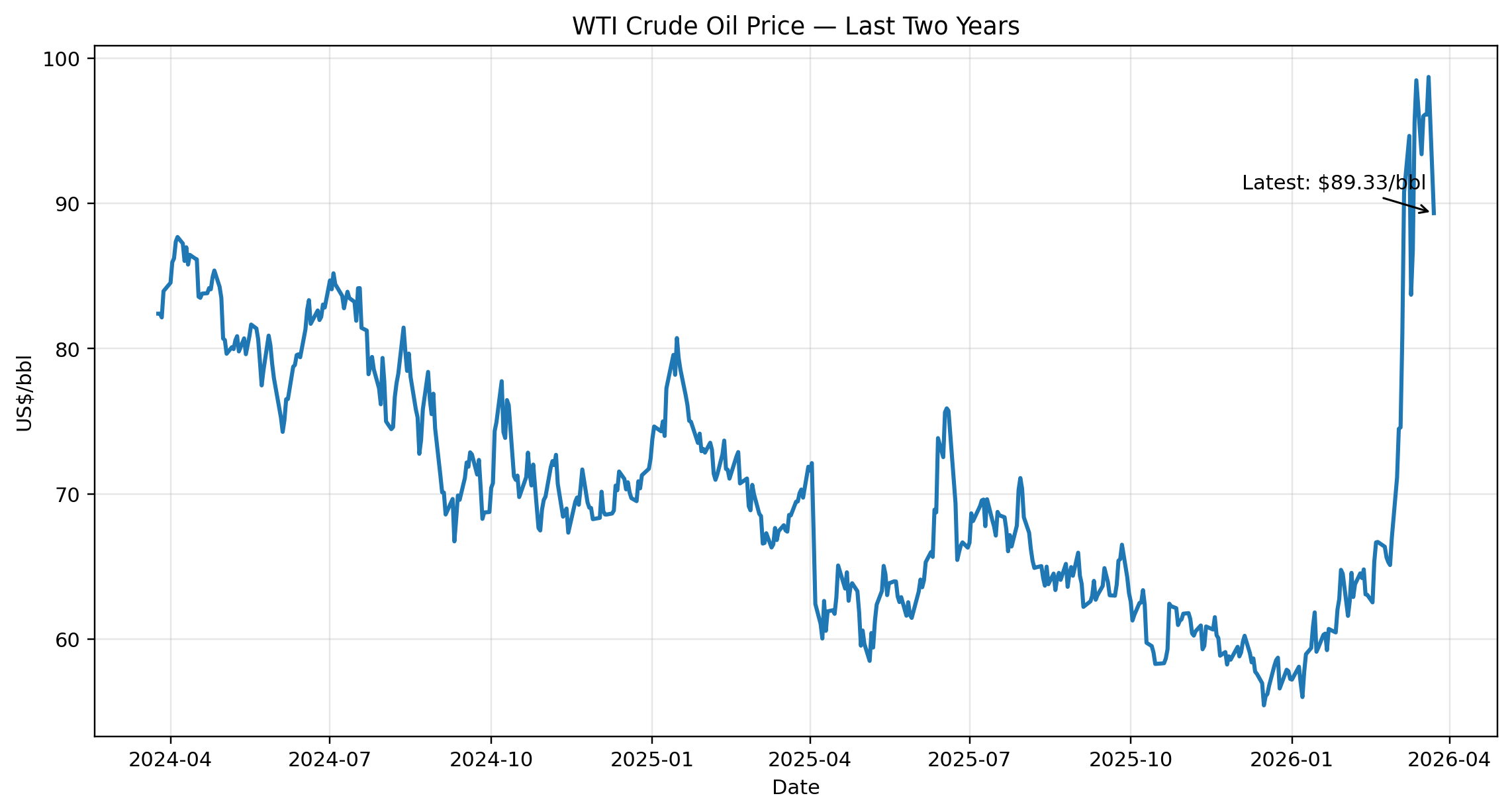

MARKET PULSE

Why higher oil prices still have not sparked a full shale response

Oil prices have moved higher in recent weeks, but the industry’s reaction has been far more restrained than many would have expected in past cycles. The latest Dallas Fed Energy Survey showed activity improving in the first quarter, yet many producers said they still have not materially changed their drilling plans for 2026. That restraint says a lot about where the industry is today. Operators are no longer responding to every price move with an immediate push for growth. They are waiting to see whether stronger prices can hold.

That caution becomes even more meaningful when viewed alongside the latest outlook from the U.S. Energy Information Administration. In its March 2026 Short-Term Energy Outlook, the EIA raised its near-term assumptions but still forecasts WTI crude oil to average about $74 per barrel in 2026 and about $61 per barrel in 2027. In short, the agency sees current strength in the market, but it also expects growing global oil inventories to put pressure on prices over time.

Taken together, the message is fairly clear. Today’s stronger oil price is helping sentiment, but it has not yet changed the industry’s broader mindset. Producers appear to be asking a more disciplined question than they did in earlier shale cycles: not whether prices are attractive today, but whether they will remain supportive long enough to justify changing multi-quarter capital plans. That is a very different posture than the rapid-growth mentality that often defined the last decade.

For royalty investors, that distinction matters. Higher prices can still provide a welcome lift to near-term cash flow, but the bigger story is that disciplined operators are continuing to prioritize capital efficiency, balance sheet strength, and long-term returns. In this market, that may be the more important signal.

Commodity | Current Price ($) | Daily Change |

|---|---|---|

WTI Oil ($) | 104.30 | +4.661+4.68% |

Henry Hub Gas ($) | 2.88 | -0.14 -4.69% |

Current Rig Count(US lower 48) | Week Change | Year Change |

543 | -9 | -49 |

*Prices are as of 03/30/2026 and sourced from oilprice.com. Rig data is provided by WellDatabase.com and as of 03/30/2026.

ROYALTY SPOTLIGHT

The difference between current cash flow and future inventory value

One of the easiest ways to misunderstand a royalty asset is to look only at the size of today’s revenue check. Current cash flow matters, of course. It tells you what the asset is producing right now, how recent wells are performing, and what commodity prices are doing in the near term. But in many cases, that is only part of the story.

The deeper value of a royalty position often lies in what has not been developed yet. If there are undrilled locations, additional benches, or future development phases still ahead, the asset may hold meaningful upside beyond its current production base. That future inventory can become increasingly valuable when it sits in a strong basin, under a capable operator, and within an area where geology continues to improve through time.

This is why royalty investing is not just about buying income. It is also about buying exposure to future drilling activity without taking on the cost and operational burden of drilling the wells yourself. A property with modest current cash flow but a long runway of undeveloped locations may ultimately be more attractive than one with stronger current production but little remaining inventory.

For investors, the key takeaway is simple: today’s cash flow shows what the asset is doing now, but future inventory helps define what the asset may still become. The best royalty opportunities often combine both the existing production that supports current income, and undeveloped upside that can refresh value over time.

Real Assets. Real Income. Real Alignment. |

BASIN FOCUS

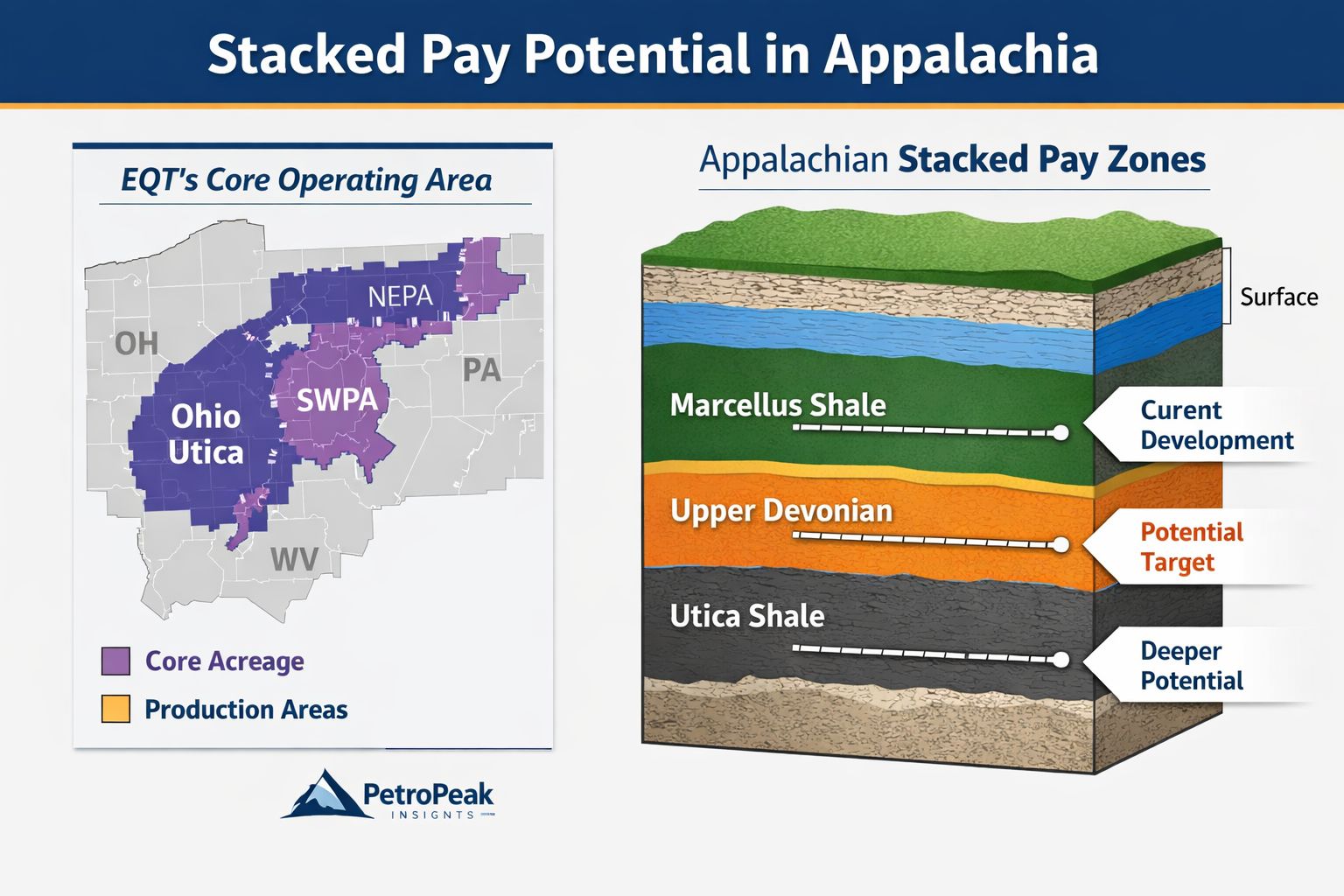

Stacked pay in Appalachia: value beyond the first bench

Appalachia has long been viewed through the lens of the Marcellus, but recent commentary from EQT suggests the story may be broadening. The company is actively delineating stacked-pay potential across additional zones in the basin, with the goal of de-risking more intervals and extending economic inventory beyond the core development horizons investors already know well. That matters because basin value is not defined only by what is producing today, but by how much future development can be unlocked across the same acreage position.

For royalty owners, this is an important concept. A mineral position tied to a strong operator and a geologically layered system may hold more long-term optionality than headline production alone would suggest. If an operator can move from a single-zone development story to a multi-zone story, the result can be more drilling inventory, more development windows, and potentially a longer runway for future royalty cash flow.

This idea of targeting multiple productive zones is not new to the industry. What changes over time is the level of understanding, confidence, and economic viability within a specific play. In many of the country’s best basins, value has expanded as operators moved beyond the original headline target and proved up additional intervals. The Eagle Ford evolved to include both the Eagle Ford and Austin Chalk, the DJ Basin has long benefited from Niobrara and Codell development, and the Permian continues to deepen as operators move across the Spraberry, Wolfcamp, and now increasingly test the Woodford. The same multi-zone concept is also well established in Oklahoma’s SCOOP and STACK and in the Uinta Basin. Appalachia may now be following a similar path, where the opportunity is not the invention of a new idea, but the continued refinement of how much resource can ultimately be captured from a known and highly productive system.

That theme also connects well to the broader gas market backdrop. EQT has been pointing to improving Appalachian pricing support from both LNG and power demand, which reinforces the idea that stacked-pay delineation is not just a science project. It is part of a larger effort to position the basin for a deeper, more durable demand cycle.

INVESTOR ADVANTAGE

Why disciplined operators may create better royalty outcomes than aggressive growth operators

In mineral and royalty investing, investors do not need operators to grow production as fast as possible. They need operators to allocate capital wisely, protect margins, and drill high-return locations that sustain asset value over time. That is why operator discipline can be a meaningful advantage for royalty owners. A company that resists the temptation to overspend during a volatile market often preserves more long-term value than one that aggressively chases short-term volume.

SM Energy’s 2026 outlook offers a good example of that mindset. The company explicitly framed its plan around maximizing free cash flow, strengthening the balance sheet, increasing shareholder returns, and adjusting activity levels to improve capital efficiency. That is exactly the kind of language royalty investors should pay attention to. It suggests an operator is focused on developing its best inventory with a return-oriented mindset rather than forcing growth for growth’s sake.

For PetroPeak’s investment thesis, that distinction matters. Strong royalty outcomes are often driven less by the most aggressive operator and more by the most rational one. When experienced operators high-grade capital, prioritize returns, and preserve flexibility, royalty owners can benefit from a more resilient stream of cash flow and a more durable asset base underneath the investment.

LOOKING AHEAD

U.S. gas is gaining strategic value from two directions: AI power demand at home and LNG pull abroad

The next phase of the natural gas story is becoming easier to see. On one side, domestic power demand is rising as AI-driven data center growth pushes utilities and grid operators to plan for meaningfully higher electricity consumption. The EIA has indicated that faster-than-expected data center expansion could lift fossil fuel generation, with natural gas playing a central role in meeting that load. Reuters also reported record-setting U.S. power demand projections for 2026 and 2027 as AI and electrification continue to expand.

On the other side, LNG export demand continues to add another layer of pull on U.S. gas. Golden Pass LNG, the ExxonMobil-QatarEnergy joint venture in Texas, produced its first LNG on March 30 and expects its first cargo in the second quarter. While Golden Pass is not a pure Permian outlet, it is a meaningful addition to Gulf Coast gas demand and another reminder that U.S. gas is increasingly tied to global markets as well as domestic power needs.

Taken together, these trends reinforce a simple point: natural gas is no longer just a commodity story tied to weather or short-term storage. It is becoming a strategic fuel for both digital infrastructure and global energy security. For royalty investors, that does not eliminate volatility, but it does strengthen the long-term case for owning assets tied to prolific gas systems and high-quality operators with access to growing end markets.

Ways to Connect with Us:

Email: [email protected]

Website: www.petropeakinvest.com

Schedule a Call: Book a time here

Follow us on LinkedIn and socials: PetroPeak Investments LLC, @petropeakinvest

Whether you’re exploring royalties for the first time or looking to deepen your exposure, PetroPeak can guide you through every step from understanding the asset class to participating in high-quality, cash-flowing deals.

Because at PetroPeak, it’s about more than just investing. It’s about building long-term income you can count on.